Becoming parents changes the way a couple sees money. Before a child arrives, financial plans typically comprise of short term desires like travel, gadgets, savings, home upgrades, or improving lifestyle. But once a child is born, everything about money suddenly feels more purposeful. Now, the question is no longer “What do we want?” instead “What kind of future do we want our child to have?”

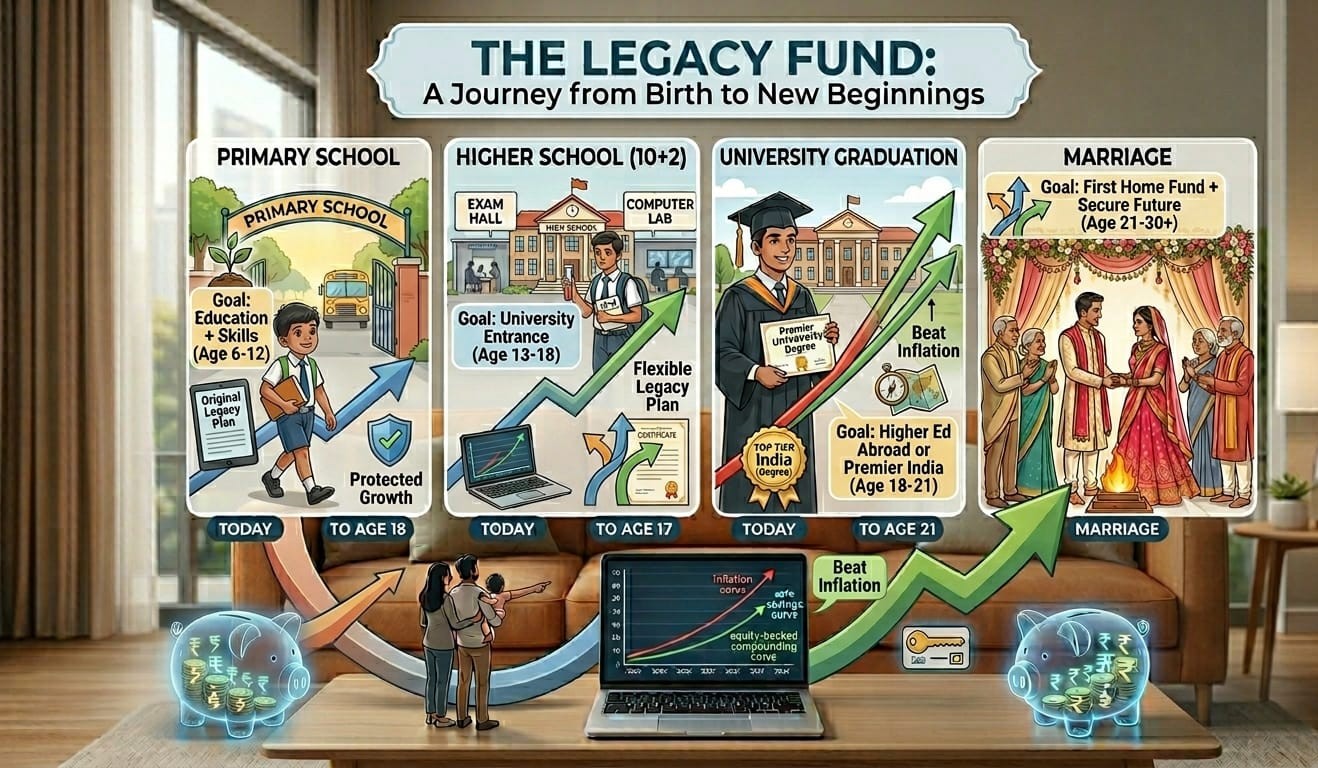

Legacy fund is a structured, thoughtful, long term investment plan designed to support a child’s milestones like education, skill development, healthcare, marriage, first home fund, entrepreneurship capital, it’s the safety cushion that makes sure your child never has to start from scratch. Let’s begin the journey of building a Legacy Fund so that by the end of this article, you’ll be able to customise a plan tailored to your needs and aligned with the age at which you’re starting this fund.

1. Understanding the Need of a Legacy Fund

A Legacy Fund is not just another savings account. It is a multi goal financial system built with longevity, protection, and compounding in mind. It usually includes a mix of

- Equity (Mutual funds, ETFs)

- Debt (bonds, fixed deposits, debt funds)

- Gold (gold ETFs, gold mutual funds)

- Insurance (term plans for parents)

- Skill-development funds

- Emergency and healthcare protection

1.1: Why couples struggle to plan their child’s future

Most parents want to start investing early for their kids, but fail to do so due to various reasons. You might feel like you need a huge amount of money just to begin, or you might get so overwhelmed by all the different options that you end up doing nothing at all. There’s also a habit of underestimating how much things like college tuition will actually cost by the time they grow up. Between waiting for the “perfect” moment and worrying about picking the wrong fund, the first step just keeps getting delayed while inflation does its work of eating up the savings.

1.2: The three pillars of a good Legacy Fund

A strong Legacy Fund has the following features:

- Growth- A strong Legacy Fund prioritizes growth, ensures that the investment beats inflation and builds significant long term wealth through the power of compounding.

- Protection- It ensures that the child’s future stays secure, even if something unexpected happens to the parents.

- Flexibility- A good legacy fund must be able to adapt and evolve as life goals and financial needs change over time.

2. How Much Money Should You Target for Your Child’s Legacy Fund?

Before choosing investments, couples must answer this fundamental question: “How much money will your child need by the age of 18 or 25?” As different goals require different investment amounts lets have a deeper look into it.

2.1: The Cost of Raising a Child Until Age 21

When inflation is factored in following is the estimated cost:-

- Middle class upbringing: ₹45–65 lakh

- Education + extracurricular: ₹35–80 lakh

- Healthcare over 21 years: ₹5–8 lakh

- Miscellaneous: ₹10–15 lakh

Total Estimate: ₹1–1.5 crore. This does not include higher education abroad

2.2: Higher Education Cost Projection

Taking into account the inflation in India which is around 8-12% following can be the cost:-

- Engineering: ₹50- 80 lakhs

- Medicine (private): ₹90 lakhs- 2 crore

- MBA (top institutes): ₹90 lakhs- 1.2 crore

- Arts/Commerce/Science degrees: ₹10–20 lakhs.

you are planning to get your child a degree from abroad then the expenses can be as follows:-

- US Graduate Degree: ₹2 crore– ₹5 crore

- Europe: ₹1 crore–3 crore

- Canada/Australia: ₹1 crore–4 crore

2.3: The Minimum Amount That You Should Target

Even if parents cannot plan for every possible future cost, the minimum Legacy Fund target should be:-

- ₹70–80 lakh for basic support

- ₹2–3 crore for comfortable support

- ₹5 crore+ for high-ambition child goals (abroad education, entrepreneurship capital)

2.4: How Early Investing Reduces Stress

If a couple starts investing when the child is born then their investments can look like this:

If you start late (child is 5 or 10), you will need to:-

- Invest more monthly

- Add lump sums periodically

- Use more equity exposure

So, the earlier you start, the easier it becomes to accumulate the target fund.

3. How to Structure a Legacy Fund

A well designed Legacy Fund includes multiple financial layers that work together to give the desired results.

3.1: The Core Four Components

- 60% Equity (Primary Growth Engine) A well designed Legacy Fund allocates almost 60% to equity, which serves as the primary long term growth engine. Equity helps the portfolio to consistently beat inflation and accumulate substantial wealth over time. This portion can be built using simple yet powerful products such as index funds (Nifty 50, Nifty Next 50), flexi cap funds, large & mid cap funds, equity ETFs, and small cap funds. Over a long horizon, this equity block typically aims to generate 10–14% returns, making it the most important contributor to the fund’s growth.

- 20–25% Debt Funds (Stability + Safety)The next allocation of say 20–25% should be in debt instruments, which act as the portfolio’s shock absorbers. Debt provides stability, reduces volatility, and ensures predictable returns even when markets fluctuate. Suitable options in this category include government securities, target maturity funds, corporate bond funds, Public Provident Fund (PPF), and laddered fixed deposits. Over time, this segment aims to deliver 6–7.5% while keeping the overall allocation steady and resilient.

- 10–15% Gold (Hedge + Diversification)For additional diversification, 10–15% of the Legacy Fund should be allocated to gold, which acts as a hedge during global uncertainty and market corrections. Gold has historically shown low correlation with equity, making it an effective stabilizing asset in long-term portfolios. The most efficient ways to invest in this segment is Gold ETFs, as they offer transparency and ease of management. Over a 15-year horizon, gold typically delivers 7–9% returns, adding a protective layer of balance to the overall fund.

- Protection Layer (Insurance + Legal Arrangements)The final and the most important component is the protection layer, which safeguards the family and the child’s future regardless of market conditions. This includes having a solid term insurance plan for both parents to ensure income continuity, along with comprehensive health insurance to cover medical risks without affecting long-term savings. In addition, proper legal arrangements such as creating a will, updating nominations, and maintaining clear documentation ensures that the legacy is transferred smoothly and securely. These protections form the foundation that keeps the Legacy Fund resilient and future proof.

3.2: A Sample Allocation for Different Risk Profiles

Conservative Parents:

- 40% Equity

- 40% Debt

- 20% Gold

Moderate Parents:

- 60% Equity

- 25% Debt

- 15% Gold

Aggressive (Early-Starting Young Couples):

- 75% Equity

- 15% Debt

- 10% Gold

3.3: Single vs. Multiple Legacy Funds

Some parents choose one combined fund. Others create goal specific mini funds:-

- Education Fund

- Skill Development Fund

- Medical Safety Fund

- Entrepreneurship/First Home Fund

There’s no one correct method, you can choose based on personality and comfort.

4. The Best Investment Instruments for a Child’s Legacy Fund

Lets have a look at the various investment instruments available to build a strong and suitable legacy fund.

4.1: Equity Instruments

- Index Funds: Index Funds are a type of Mutual Fund that replicates a market index. These funds do not aim to outperform the index instead mimic the index to produce similar returns. These are cheap with relatively lower risk and thus are the most reliable way to grow a child’s money over 20 years.

- Flexi Cap Funds: Flexicap Funds are equity Mutual Funds that offer the fund manager flexibility to invest in any market cap. Here fund manager can move the funds across large, mid and small cap as per his judgement

- Equity ETFs: Equity ETFs (Equity Exchange Traded Funds) are investment funds that buy a basket of stocks and trade on the stock exchange just like a normal share. They usually track a stock market index.4. Small Cap FundsThis is the high growth part of the plan. You invest in small companies that could become giants. The price jumps around a lot. They are risky instruments but are fine for a 15 year goal where you want the biggest returns.

4.2: Debt Instruments

- Public Provident Fund (PPF): The Public Provident Fund (PPF) is a government backed reliable long term investment option having a 15-year lock in period and offering some of the highest tax free returns available in India. It is suitable for conservative investors who want secure, steady growth for long term goals, especially when planning financial support for a child’s future.

- Sukanya Samriddhi Yojana (SSY) for girl child: The Sukanya Samriddhi Yojana (SSY) is one of the safest and best government backed investment schemes for a girl child. It offers the highest interest rate among all the available small savings options along with completely tax free returns. If you want to know more about SSY, check our detailed article on it.

- Target Maturity Funds: Target Maturity Funds offer a fixed maturity date, making them a dependable option for investors who want clarity on when their money will be available to them. These funds carry lower risk because they invest mainly in high quality government and corporate bonds aligned to a fixed timeline.

4.3: Gold Instruments

- Gold ETF: A Gold ETF is a convenient and liquid way to invest in gold without having to deal with physical storage or purity concerns. It allows you to track gold prices while buying and selling units on the stock exchange. This makes Gold ETFs an efficient and hassle free tool for adding gold exposure to a long term investment portfolio.

4.4: Protection Instruments

- Term Insurance for Parents: Term insurance for parents is essential because a child’s future should never depend on financial uncertainty. Both parents must be adequately protected with a pure term plan that provides at least 15 times their annual income as coverage, ensuring long term security for the family. Adding important riders like accidental and critical illness enhances the policy and ensures that the child’s future remains safeguarded even in unexpected situations.

- Health Insurance + Super Top-Up: Having a strong health insurance plan along with a super top-up is essential because medical emergencies should never force the parents to break their Legacy Fund which is meant for their child’s future. A comprehensive health cover ensures that sudden hospital expenses are managed smoothly, allowing the family’s long term investments to stay intact and continue growing without interruption.

5. How to Start Building the Legacy Fund (Step-by-Step Guide)

Step 1: Set Your Target

Choose your Legacy Fund goal:

- ₹50 lakh

- ₹1 crore

- ₹2 crore

- ₹3 crore+

Then determine SIP amount.

Step 2: Decide Your Monthly Contribution

You can start with whatever amount you can manage, even a small SIP of ₹2,000 per month is a meaningful beginning. As your income grows, increase this SIP by around 10% every year to accelerate your wealth creation. This simple habit of gradual, consistent step up investing can significantly boost compounding power and ultimately double the final corpus over the long term.

Step 3: Choose the Right Mix of Instruments

Create a structured monthly investment plan consisting of:

- 3-4 equity funds

- 1 debt fund

- PPF for stable long-term debt

- Term insurance for parents

Step 4: Automate Everything

Automating your entire investment process is one of the most effective ways to stay consistent, as manual investing often leads to skipped months and irregular habits. You should set up automatic SIPs, bill payments, and insurance renewals so they run smoothly without needing your attention. You can even automate reminders for your annual portfolio review, ensuring that your Legacy Fund stays on track with minimal effort and zero missed opportunities.

Step 5: Review Only Once a Year

Review your Legacy Fund only once a year, because excess monitoring can create unnecessary panic and can lead to bad decision making. During this annual check, focus on a simple yet effective checklist:

- Evaluate your fund’s performance

- Check for any allocation drift

- Track your progress toward the goal

- Adjust your SIP amount if needed.

This disciplined, annual approach keeps you informed without letting short term market noise distract you from long term success.

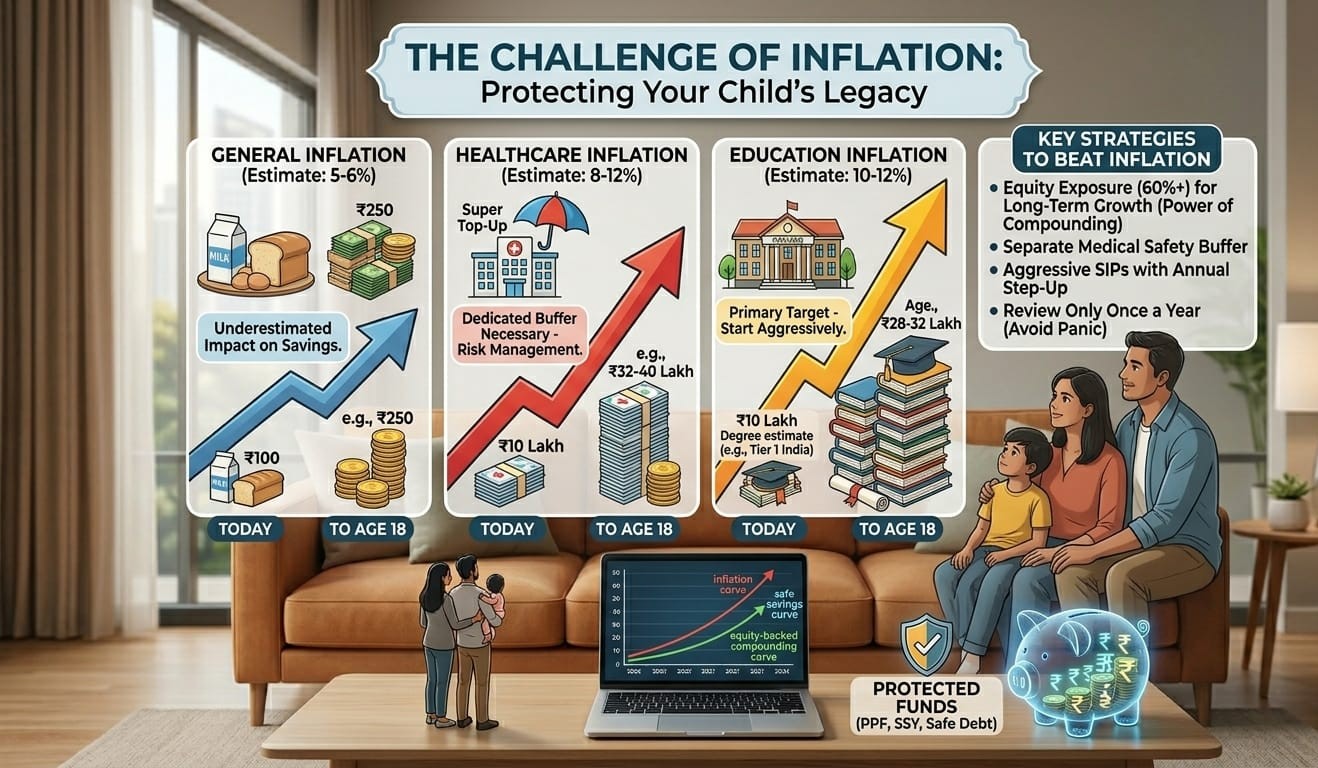

6. Inflation and the Future

People generally underestimate the impact of inflation.

6.1: Education Inflation

Education inflation in India rises at almost twice the rate of general inflation, which makes future costs significantly higher than most parents expect. While normal inflation averages around 5–6%, education inflation typically ranges between 10–12%, causing fees to increase rapidly over time. This means a degree that costs ₹10 lakh today could easily require ₹28–32 lakh in the next 18 years, highlighting the importance of early and aggressive planning for a child’s education.

6.2: Healthcare Inflation

Healthcare inflation is rising rapidly, with medical costs increasing by 8–12% every year, making treatments significantly more expensive over time. Thus it’s essential for parents to maintain a dedicated medical safety buffer specifically for their child. This ensures that any unexpected health issue can be managed without disrupting long term investments or compromising the Legacy Fund.

6.3: Cost of Skills + Career Development

Over the next 20 years, careers will evolve dramatically, and your child may need significant investment in skill building and career development to stay competitive. This could include online certifications, Ai focused courses, robotics training, international exchange programs, or even initial capital to explore entrepreneurship. You must ensure that your child is financially prepared for such opportunities, no matter how the future changes.

7. Protecting the Legacy Fund (Legal + Risk Management)

This chapter covers how to ensure the Legacy Fund is untouched, protected, and passes safely to the child.

7.1: Nomination & Will

Establishing proper nomination and a simple will is essential to ensure that your child’s financial future remains secure and well organized. Parents should add their child as a nominee or secondary nominee wherever need arise, create a straightforward will outlining asset distribution, and maintain clear documentation of all investments. Storing important digital proofs in an accessible and secure place ensures that the Legacy Fund transfers smoothly without confusion or legal complications.

7.2: Avoid Using Child’s Money for Adult Emergencies

Many parents unintentionally derail their child’s financial future by dipping into the Legacy Fund during adult emergencies, which is one of the most common mistakes. It’s crucial to ensure that this fund is never touched for EMIs, travel expenses, family functions, personal luxuries, or demands from relatives. To avoid such situations, parents must maintain a separate emergency fund dedicated solely to adult needs, allowing the Legacy Fund to grow undisturbed and serve its true purpose.

7.3: Insurance is Mandatory

Insurance is absolutely mandatory because it forms the foundation of any solid child investment plan. Without a proper term insurance policy in place, a family can face severe financial strain during unforeseen events, which may force parents to break or deplete the Legacy Fund. A strong insurance cover ensures that the child’s long-term goals remain protected, regardless of life’s uncertainties.

8. Teaching Your Child About Money

Your Legacy Fund is incomplete unless your child knows how to handle wealth responsibly.

8.1: Start Financial Literacy Early

Teach concepts such as:SavingSpending wiselyInvestingDelayed gratificationUse small examples and stories.

8.2: Create a Mini Investment Account for the Child

Creating a mini investment account for your child can be a powerful way to cultivate financial awareness as they grow, especially after the age of 10–12 years. You can start by giving them a small monthly allowance and teaching them how to budget and track their spending. After that gradually introduce them to simple investment concepts through index funds and show them how compounding works using real charts. This hands on experience helps build strong financial habits early in life.

8.3: Encourage Skills That Support Financial Independence

Like:

- Coding

- Communication

- Creative skills

- Problem-solving

- Entrepreneurship thinking

9. Couples Starting Late – What to Do?

Many couples start when the child is already 5, 10, or even 15 years old.

9.1: If Starting When Child is 5

If you’re starting the Legacy Fund when your child is already 5 years old, you’ll need to take a slightly more aggressive approach to make up for the lost early years. Increasing your equity exposure to around 70% can help accelerate long-term growth through compounding. Additionally, make sure to boost your SIP amount by about 15% every year to strengthen your corpus and keep pace with rising future expenses.

9.2: If Starting When Child is 10

When starting later, it becomes important to strengthen the portfolio through safer yet effective strategies. Adding lumpsum contributions whenever possible helps speed up the growth and compensate for the shorter investment horizon. You should stay away from high risk smallcap funds, as they are volatility and can hamper investment due to availability of less time. Instead, you should choose target maturity debt funds that align with your child’s expected college year, ensuring stability and timely availability of funds.

9.3: If Starting When Child is 15

If you begin planning when your child is already 15, the focus should shift towards capital protection and timely availability of funds. In such cases you should prioritize extra safe debt instruments and keep equity exposure low to minimize volatility. Fixed deposits that are timed to mature around the child’s college admission years can provide stability, and if required, education loans can help fulfil the gaps without compromising financial security.

10. Common Mistakes Parents Make (and How to Avoid Them)

- Mistake: Investing randomly without a plan leads to confusion and inconsistent results.

- Solution: Follow a structured allocation to keep your investments organized and aligned with long term goals.

- Mistake: Mixing emergency funds with the child’s Legacy Fund reduces long term growth and creates financial instability.

- Solution: Keep both funds completely separate to maintain clarity and protect the child’s future.

- Mistake: Stopping SIPs during market corrections disrupts compounding and slows long term growth.

- Solution: Continue your SIPs, as corrections create excellent opportunities to buy at lower prices.

- Mistake: Chasing short term returns leads to impulsive decisions and unnecessary risk.

- Solution: Stick to a disciplined long term strategy to build stable and consistent wealth.

- Mistake: Buying child insurance plans results in low returns and unnecessary costs.

- Solution: Avoid these plans and focus on higher return, low cost investment options instead.

Conclusion: Your Child’s Future Starts TodayA Legacy Fund is the strongest, most impactful gift a couple can give their child. It builds independence, confidence, security, and a launchpad for life.You don’t need wealth to start building a legacy.You just need consistency.Whether you start with ₹2,000 or ₹20,000 per month—Start today.

For regular personal finance related updates do follow us on Facebook and Instagram

For any queries do Contact Us